The appraisal files that move most efficiently are rarely the ones that are simply marked urgent. They are the ones that arrive complete, clear, and realistic from the start.

For brokers, that distinction matters. Turnaround time is often shaped before the file reaches the appraiser: by how complete the order is; the documents provided; the property details disclosed; the client expectations set; and the quality of the instructions attached to the file.

In a tight financing timeline, even small gaps can create avoidable friction. An incorrect postal code, a missing purchase agreement, unclear rental instructions, a property access contact who is difficult to reach, an undisclosed secondary dwelling, or an unrealistic value expectation can slow a file down when the client expects momentum.

Below are several common areas where appraisal files can lose progress and how brokers can keep them moving to avoid delays.

A rushed order is not a faster order

One of the most common sources of appraisal delay is also one of the easiest to avoid: incomplete or inaccurate information at the time the order is submitted.

While it might sound like a given, the address and postal code need to be correct from the start. These are not just administrative details; they help confirm the exact property and assign the appropriate local appraiser. A small error can send the file in the wrong direction before the appraisal work has begun.

On purchase files, the agreement of purchase and sale should be uploaded with the appraisal order whenever possible. The appraiser needs it to confirm key details such as purchase price, closing date, property terms, and any conditions or context that may affect the assignment. In some cases, much of the analysis can be completed, but the report cannot be finalized until the purchase agreement has been reviewed.

The same principle applies to MLS® listings, renovation details, rental information, floor plans, condo or strata documents, tax details, builder documents, renovation invoices, permits, surveys, and any other material that helps explain the property or assignment. Not every file needs every document. But when the information is relevant, it should be provided upfront — not after the appraiser has to ask for it.

Special instructions should remove ambiguity

The most useful special instructions are not long; they are specific.

A common example is market rent. Brokers may note that the lender requires a full appraisal “with rent,” but that does not answer the appraiser’s real question: rent for what?

Is the lender asking for market rent for the full property? A legal basement apartment? The upper unit only? A laneway suite? A garden suite? That distinction can affect the scope of work and the analysis required.

A clearer instruction, such as “Lender requires market rent for the legal basement apartment,” gives the appraiser the information needed at the outset and reduces unnecessary back-and-forth.

The same applies to secondary dwellings, recently completed additions, mixed-use characteristics, income-producing components, unusual access, and other non-standard property features. The appraiser should not be discovering those details for the first time on site.

Dates and access details drive the file

Indicating when the appraisal needs to be completed is helpful, but it is not the only timing detail that matters. For a home purchase, brokers should include the purchase and sale agreement, which includes the closing date, so the file can be prioritized in context.

Those dates are especially important when the property is difficult to access, tenanted, remote, under renovation, or likely to require additional analysis. A tight deadline on a straightforward urban property is one thing. A tight deadline with tenant coordination, unusual access, or limited comparable sales is another.

Access is one of the simplest variables brokers can influence. Where possible, provide more than one contact name and more than one phone number or email address. If the only contact is unavailable or slow to respond, scheduling can stall immediately.

For tenanted properties, provide the tenant contact at the time of order and make sure the borrower or realtor is prepared to give proper notice. A file can be ready from a valuation perspective and still lose time because no one can access the home.

Brokers should also flag practical barriers that may affect communication or inspection scheduling, including language, mobility, or technology access challenges. These details do not need to be over-explained. They simply need to be known early enough for the appraiser to plan around them.

Renovation details need to be shared before the appraiser completes the valuation

On refinance files, brokers can add real value by helping clients identify meaningful improvements before the appraisal is ordered.

Appraisers will observe the property, but they may not know when work was completed, what was invested, or whether certain upgrades are above the typical standard for that market. A renovated kitchen, updated bathrooms, heated floors, high-end materials, basement finishing, or major functional improvements can all help the appraiser understand the property more accurately.

Renovation status is especially important. A planned renovation, in-progress renovation, and recently completed renovation may require different appraisal treatment. If that information is missing or unclear, the file may need to be clarified before it can proceed properly.

This does not mean every minor repair needs to be listed. But when the owner has made substantive improvements, the broker should make sure that information is provided upfront rather than after the value comes in lower than expected.

Checklist for documents and information required when creating an appraisal order

Clients should be ready before the inspection call comes

For full appraisals, a conversation with the client beforehand can prevent delays. The homeowner should know that the appraiser will need interior and exterior access, and that missing the appointment can lead to delays and potential additional fees. They should also have relevant documents available, such as tax bills, title documents, surveys, renovation invoices, building permits, and any other materials that help explain the property.

The practical details matter. Gates, sheds, side entrances, and other exterior access points should be unlocked. The home should be reasonably accessible inside, with obstacles cleared near the electrical panel, furnace, utility rooms, and other areas the appraiser may need to view. Pets should be secured. If tenants are in place, they should receive proper notice.

These steps help to reduce avoidable roadblocks so the appraiser can complete the inspection efficiently and the file can keep moving. RPS also offers a homeowner’s guide to help clients prepare for an appraisal appointment.

Value expectations should be reset early

In the current market, one of the biggest disconnects between what borrowers believe their property is worth and what current comparable sales support.

Many clients still anchor expectations to a neighbour’s sale from two years ago, a peak-market purchase price, or an informal estimate that has not been tested against today’s market. That becomes a problem when the broker enters an estimated value based largely on the client’s opinion and the appraisal later comes in materially lower.

The better conversation is not, “What do you think your home is worth?” It is, “Let’s look at what the current market is supporting.”

RPS tools such as the House Price Tracker can help brokers frame that discussion using appraisal comparables. It is not a lender-accepted appraisal or a substitute for an AVM, but it can give the broker and borrower a value range. This helps to create a more grounded starting point before the file is ordered.

That early conversation can prevent a much harder one later. If the appraised value comes in below the borrower’s expectation, the impact may flow through to loan-to-value, down payment requirements, lender options, or the overall financing structure. A client who understands that possibility before the appraisal is ordered is easier to advise than one who hears it for the first time after the report is complete.

Timelines should reflect the property

Some properties are complex or remote, and therefore may require more time for the appraisal to be completed.

Urban properties in well-covered markets are usually easier to schedule because appraiser coverage is deeper and access is often more straightforward. Remote homes, cottage properties, island properties, ferry-access properties, unique homes, new builds, private sales, mixed-use properties, and homes with limited comparable sales may require more time.

This is less of a service issue and often a scope, access, coverage, or diligence issue.

Brokers can reduce client frustration by setting that expectation early. A remote or non-standard property may take longer, even when the file is urgent. It is better to let the client know that at the beginning.

The same applies to files that begin as a desktop or drive-by appraisal but need to be upgraded. If there is not enough reliable information to complete the lower-scope valuation, a full appraisal may be required. Clients should understand that possibility before they receive a call from an appraiser asking to inspect the property.

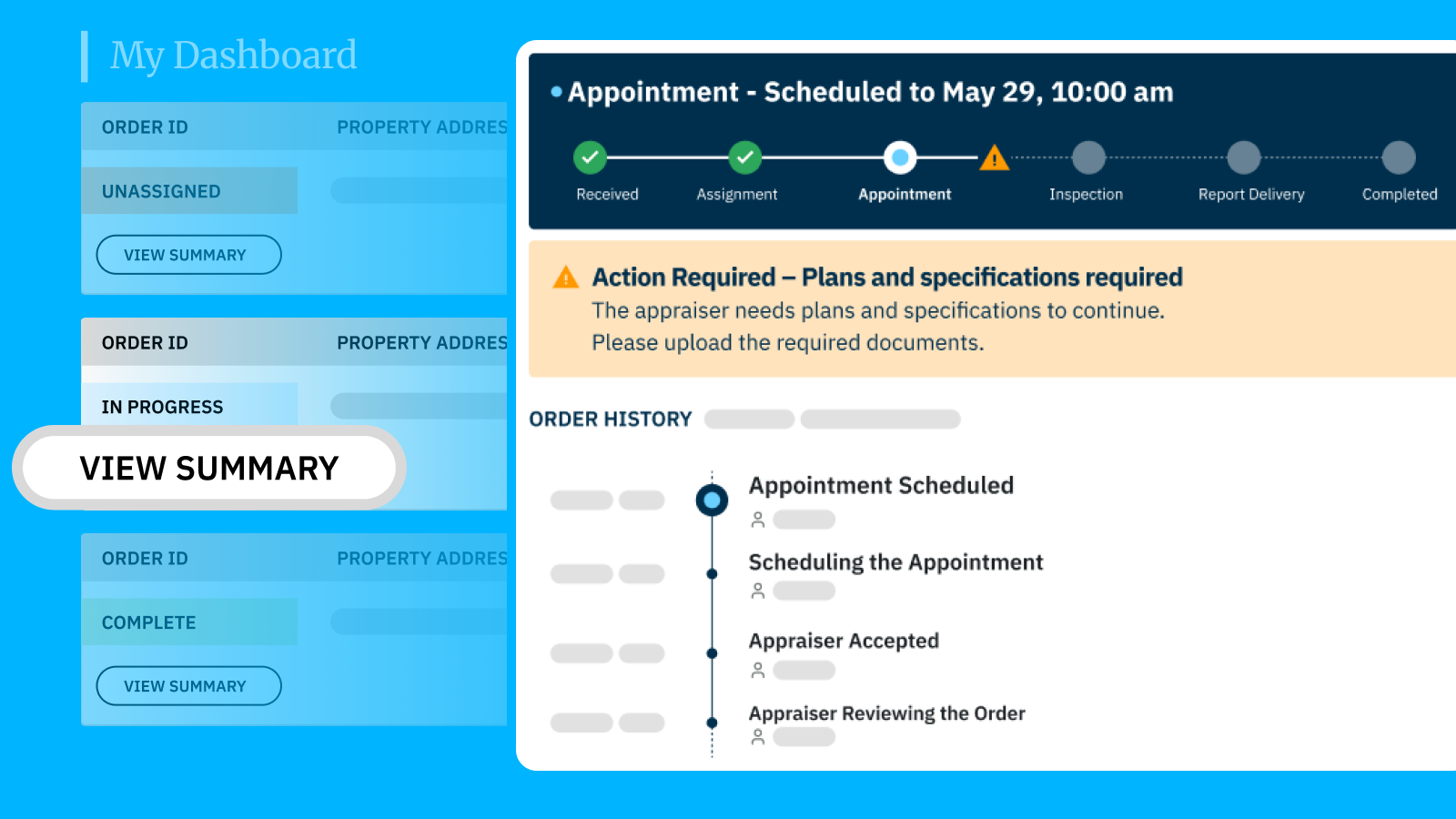

Track My Order helps brokers manage issues earlier

Visibility is one of the most useful tools a broker can have once the appraisal is in motion.

RPS’s Track My Order tool gives brokers status visibility from order placement through completion. Once enabled, the order submitter receives a tracking link with each order, allowing the team to check progress without contacting support for routine updates.

The tracking page can show where the file stands and whether issues such as missing documents or difficulty reaching contacts may be causing delays. For brokers, that visibility can make client communication more practical. Instead of waiting until a delay has already affected the financing timeline, the broker can see where the bottleneck is and help address it earlier.

Track My Order serves as a file-management tool, not just a convenience feature.

“RPS’s Track My Order feature gives brokers status visibility from order placement through completion. Once enabled, the order submitter receives a tracking link with each order, allowing the team to check progress without contacting support for routine updates.”

Redirects move faster when the release is ready first

Lender redirects are another area where small process gaps create predictable delays.

If an appraisal was completed for one lender and the deal later needs to move to another, the broker may request a redirect or letter of reliance. But before that can proceed, RPS typically requires a release letter from the original lender.

Too often, the redirect request is opened before that release has been obtained. The result is a preventable back-and-forth: RPS identifies the missing release, the broker has to go back to the original lender, and the original lender may not treat the request as urgent because the deal is no longer proceeding with them.

The smoother approach is to obtain the original lender’s release before opening the redirect request. That keeps the file moving and avoids putting the broker in a reactive position.

A low appraisal needs evidence, not opinion

An appraisal that comes in lower than expected does not automatically end a file, but it does change the conversation.

If the original product was a desktop or drive-by appraisal, one option may be to proceed with a full appraisal. An interior inspection may capture features, condition details, or upgrades that were not available through a lower-scope product. That does not guarantee a higher value, but it can provide a more complete basis for the valuation.

If the low value comes from a full appraisal, the next step is not to dispute the number. The broker can work with the client or realtor to identify relevant comparable sales that may support a different conclusion. A larger, superior, or materially different property is not usually a stronger comparable simply because it sold for more.

A broker can also opt to appeal the decision with a formal Value Appeal. RPS offers lenders and brokers the option to appeal a value if it does not seem accurate. Helping the client understand the difference between challenging an appraisal and providing meaningful market evidence will keep the appeal focused on facts the appraiser can review and consider.

If you are managing an appraisal file where timing, documentation, property complexity, or valuation expectations are creating friction, RPS can help you understand the next step.

RPS is the go-to appraisal partner for brokers across Canada, supporting every stage of the process from file submission to value appeals.

Julian Perera

Appraiser Network Manager, Western Region

Julian is RPS’s Appraiser Network Manager, Western Region. He has extensive experience within RPS’s Broker and Success teams. As a designated DAR, Julian combines strong industry knowledge with a deep understanding of appraiser relationships, operational workflows, and service excellence.

Julian is RPS’s Appraiser Network Manager, Western Region. He has extensive experience within RPS’s Broker and Success teams. As a designated DAR, Julian combines strong industry knowledge with a deep understanding of appraiser relationships, operational workflows, and service excellence.